Finance

FG orders 24 hours ports operation

—– Okonjo-Iweala’s World Bank contest boosts Nigeria’s profile

—– Okonjo-Iweala’s World Bank contest boosts Nigeria’s profile

Concerned by the increasing cost of doing business in Nigeria, President Goodluck Jonathan has ordered 24 hours operations at the Nigerian ports in a bid to reduce the number of days for clearing goods as well as make the ports more competitive.

The coordinating minister for the economy and minister of finance Dr. Ngozi Okonjo-Iweala dropped the hint yesterday in Washington at the just concluded Spring meeting of the IMF/World Bank

The minster, who addressed the Nigerian press alongside the Central Bank of Nigeria (CBN) Governor, Mallam Sanusi Lamido Sanusi; the Governor of Anambra State, Peter Obi and Dr. Mansur Murthar Executive Director World Bank, also said that her bid for the President of the World Bank was well received by the international community and has boosted the profile of not just Nigeria but Africa as a whole.

Lamenting that Nigeria is the only country whose ports do not operate 24 hours, the Finance Minister, said that the country was losing out in terms of revenue as goods are being shipped to neighboring countries that are very efficient in the management of their ports.

“We are the only port working from 9.am to 5pm in the world. Other ports operate 24 hours and that is why their ports are cheap because importers do not have to pay for demurrage. Apart from reducing the number of agencies in the port, which we have done, we also need to remove the bureaucratic requirements.

“Besides, we need to make more investment in modern technology and machineries. So, this is what we are pushing the concessionaries to do,” she said. Corroborating the Finance minister, Governor Obi insisted that the ports concessionaires have actually not made any meaningful investment.

Noting that 60 per cent of goods shipped into West Africa are meant for Nigeria, he said it was cheaper to ship goods to Ghana than Nigeria.

He said empty containers litter the ports because once the goods in them are off-loaded, they are not reloaded for exports and the shippers would rather abandon them instead of carrying empty containers.

The Minister said that the Nigeria delegation to the Spring meetings was besieged by delegates from Africa and other emerging markets with congratulatory messages saying that her bid for the position of World Bank has altered the way the multilateral institution was dealing with the developing countries.

She said that her participation has boosted Nigeria’s image and has been very beneficial to the country since the Nigeria delegation arrived Washington.

On what Nigeria stands to benefit from the Spring meeting, the minister said that the Nigerian team came to the meeting to rob minds with others to share idea and knowledge of what is happening at the global economy to help in planning and preparing for what others are forecasting about the global economy.

She said: “It is vital for us, Nigeria does not exist in isolation, about 60 per cent of Nigeria export goes to Europe and America, so we need to hear what is happening in other economies to be able to calibrate how we might be imparted.

“What we are taking away from this meeting is that there is fragile recovery of the US economy, though there recovery is fragile, unemployment is still high above eight per cent, the Euro zone is even being more fragile, the sovereign debt crisis is still overhanging. In addition, Spain is now joining the whole configuration of countries that are having problem with sovereign debts. As you know things are very tough in Spain, unemployment is about 23 per cent and youth unemployment is 50 per cent, so one of the big economies in Europe is having problem in addition to Greece,Island and Portugal.

“So when you hear that that the global economy is fragile, US is recovering but still very difficult, that gives you information with which to calibrate what you need to do,” she said.

The minster stressed the need for Nigeria to continue the diversification of the economy; the structural reforms on power; the ports reforms; development of sources of growth in agriculture, housing as well as improving our exports of other products.

“We do not need to depend on oil only, which is sent to these economies. We need to diversify trade to Africa countries; to growing economies like India, China and Brazil and other emerging markets. These are the key message. It just reinforces the part we are already on,” she said.

Sanusi reiterated the need for structural reforms to be put in place.

“We need to protect ourselves and hedge because of the vulnerability of our economy because of oil price. This reinforces the need to save at the time when oil prices are high because if these dark clouds translate to fall in oil prices Nigeria is going to have major problems.

“The whole idea of saying let us look at the excess crude account, let us save now when prices are over $100, is basically not because we have a problem now. But if something happens and something may happened based on what we beginning to see, we are going to have problems in both the fiscal and the exchange rate sides.

“We have seen oil fall to $37 per barrel and we all know what the country went through. We will continue engaging until all the tiers of government agree that we have to safe,” he said.

-

Economy14 hours ago

Economy14 hours agoGlobal Economy Endures War Shock So Far–Georgieva

-

News14 hours ago

News14 hours agoAfreximbank cancels annual meeting on Ebola concerns

-

Agriculture14 hours ago

Agriculture14 hours agoAFC backs $7bn Dangote Fertiliser expansion to strengthen Africa’s food security

-

Economy14 hours ago

Economy14 hours agoManufacturing sector paid N329.59bn to FG as VAT; company income tax net N1.37trn in Q1 2026—NBS

-

News14 hours ago

News14 hours agoFG, States, LGs shared N2.26trn as April FAAC allocation

-

Economy14 hours ago

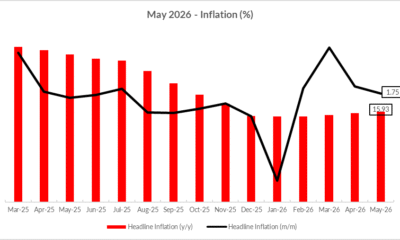

Economy14 hours agoNigeria’s inflation rate inches up to 15.93% in May, CPPE attributes rise to impact of geopolitical tensions in the Middle East

You must be logged in to post a comment Login